Is Industrial Real Estate a Good Investment in 2023?

Wellings Capital and its affiliates have been investing in commercial real estate, including mobile home parks and self-storage, for years. We added industrial real estate over the last several years, and this asset type is providing meaningful risk-adjusted returns for investors in three of our funds. This article explores our thoughts on this broad topic.

He may have been exaggerating. But it didn’t seem like it.

I was meeting with a Philadelphia industrial developer for breakfast today, and he stated that no Class B small bay/flex industrial real estate is available to rent or buy in his county.

I hear this everywhere, from Phoenix to Florida and many points between. Strategically located small bay/flex industrial space is in extremely high demand, and other industrial space types are also.

But that doesn’t mean it’s a good investment.

Internet stocks were also in high demand in 1999, and we know how that ended. In this article, we’ll explore the viability of the industrial real estate asset type, and I’ll share some things to look for as you evaluate an investment.

Industrial Real Estate Defined

Industrial real estate encompasses facilities dedicated to manufacturing, production, research and development, storage, and distribution. This may include manufacturing plants, warehouses/storage facilities, e-commerce centers, land/lots for outdoor storage and parking, flex industrial (office space in the front, warehouse in the back), and showrooms. Some industrial real estate is also called “logistics” real estate. Industrial real estate assets are typically located adjacent to key transportation hubs such as seaports, highways, rail junctions, and airports.

Some industrial assets are built to suit internally or for lease. Some are built on spec, with the hope of finding appropriate tenants. Many are repurposed from a previous use to a newer one.

As a side note, I wrote a book on self-storage where I highlighted the strategy of converting older industrial or retail buildings to self-storage. Our firm, Wellings Capital, has invested in conversions like this.

The Growth of Industrial Real Estate

The online revolution and the rapid growth of the entrepreneurial economy have spurred significant growth in the industrial real estate sector. The proliferation of e-commerce, with its broad supplier base and heightened customer demands, have strained the nation’s warehousing and logistics capabilities.

Self-storage and apartment developers have gobbled up land that might otherwise be available for industrial development. Industrial manufacturing and supply chains are building facilities closer to consumers for fast delivery and to avoid supply chain snags. This has led to a sharp rise in industrial demand.

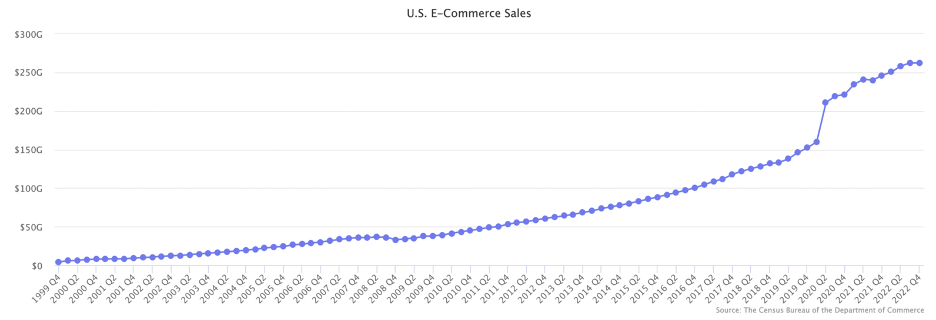

Check out the growth of e-commerce from the 90s to now…

One might expect a marginal impact on industrial since e-commerce only replaces retail sales. But e-commerce uses more space than many other types of industrial real estate. In Q2 2022, Cushman & Wakefield Director Carolyn Seltzer said:

“E-commerce fulfillment requires intense use of logistics space, often demanding three to four times the logistics space of traditional brick-and-mortar retail replenishment. Online order fulfillment necessitates higher nominal inventory levels given the product variety and the fact that parcel shipping requires much more space than palletized shipping. Furthermore, e-fulfillment often includes other value-add services such as assembly and reverse logistics.

Because e-commerce fulfillment is much more space-intensive than traditional warehousing, the long-term structural growth rate of logistics real estate has increased in tandem with the growth of e-commerce, and this is expected to continue. Digital sales soared in 2020 amid the pandemic and grew by 14.6 percent in 2021, equating to $870.8 billion being spent online.

Online sales surged more than four and a half times faster than total retail sales in 2020, growing by a staggering 31.8 percent, the highest annual growth of any year and more than double the sizeable 14.1 percent jump in 2019. That propelled U.S. e-commerce penetration as a percentage of total core retail sales to a record high of 21.9 percent by Q2 2020 at the height of the pandemic and lockdowns.”

The Pandemic Effect

While the penetration of e-commerce as a percentage of total retail sales was about 15% before Covid, CBRE estimates it will more than double to 39% by 2030. This graphic shows critical trends from pre- to post-pandemic:

Recent labor shortages and supply chain hiccups have strained logistics systems, creating potentially more demand for industrial real estate because companies tend to stock more goods onsite to avoid shipping delays. And many are building redundancy into their systems to stay competitive. We believe it’s a great time to own a stake in industrial real estate!

Did You Miss the Boat?

“If rental rates and occupancy have surged for years, maybe I missed the boat. Perhaps the natural supply and demand shift means this is not the ideal time to invest in industrial real estate.”

Capitalism facilitates this argument in most cases. I write this article in late-March 2023, amidst sharp interest rate increases and an economic slowdown. Amazon, Walmart, and other large multinational companies are laying off employees. CRE rents are flattening, and some industrial properties in some markets will undoubtedly follow suit.

Below I will share why I think industrial properties will shine for years to come. Then I will share an industrial asset strategy that should excel in almost any economy or market. These are the deals we are pursuing in 2023 and every other year.

Industrial Real Estate Supply and Demand in a Slowdown and Beyond

Real estate development retracts in slowdowns. Interest rates often rise on the front edge of slowdowns (like now). Projected ROIs for development deals are uncertain. The result is decreasing new supply.

Yet the current shift to e-commerce continues. This should exacerbate the space shortage in future years. I believe this will create an even stronger situation for industrial real estate investors. This is precisely what happened in the multifamily space post-GFC.

Picking a Winner in Almost Any Economy and Geography

Speculative real estate development creates big winners and big losers as economies expand and contract. This is not my favorite way to invest.

My firm focuses on risk-adjusted returns, which evaluate more than raw profits, but how much risk investors take to obtain those profits.

I’m in my third decade as a real estate investor, and I’ve learned a “secret” to successfully accelerate risk-adjusted returns. It’s not really a secret, but it seems like one since it is more frequently discussed than implemented.

Warren Buffett has done quite well for his investors with a similar strategy – value investing – to generate outsized returns by purchasing whole businesses or shares of businesses. Berkshire Hathaway could lose about 99% of its value and still beat the S&P 500 in the same period. Think about that.

So, what is this so-called secret? And why does it often outperform other strategies in good economies and bad, and in times of inflation, high interest rates, and economic instability?

The secret: acquire assets with significant intrinsic value…then mine that value to increase profits and value that outrun interest rate hikes and shrinking cap rates…then hold that asset until a favorable point in the economic cycle.

Intrinsic value refers to potential benefits not tapped by the current operator. Identifying and unlocking it provides a powerful opportunity to increase profits, value, and investor wealth.

Let’s detour for a quick commercial real estate value primer. While residential real estate value is based on comparable properties, commercial real estate is based on net income (NOI) and capitalization (“cap”) rates.

CRE Value = Net Operating Income ÷ Cap Rate

The cap rate is the market’s evaluation of expected unleveraged ROI for an asset like this at this location and time. Cap rates expand in times of rising interest rates or poor economic conditions because higher interest rates directly lead to lower cash flow for leveraged assets.

While the NOI is largely under the operator’s control and stems from effective acquisition and operations, the cap rate is mainly outside the operator’s control.

So, in any economy, the operator’s goal is to locate assets with intrinsic value and extract that value by increasing income. If the operator increases income enough and isn’t pressured to sell, investors may be largely immune to the value-shrinking pull of expanding cap rates in bad economies. In solid economies where cap rates are shrinking and market value is increasing, NOI growth accelerates this process.

An example of intrinsic value is highlighted in one of our self-storage investments in Colorado. It had a large vacant warehouse attached to the self-storage facility. Our operating partner cleaned up the space, performed deferred maintenance, then leased it to three tenants.

This warehouse lease raised the property’s value from its purchase price of about $11 million to almost $20 million, assuming a cap rate of 6%. The equity in the deal was just under $5 million. This is a great example of mining intrinsic value. We were quite happy to be the largest investor in this deal.

Our Favorite Industrial Real Estate Type

The industrial real estate asset class can be divided into three segments: small bay, mid bay, and large bay. Light industrial is a term usually utilized to describe primarily small bay facilities. Due to their infill location and environmentally friendly/flexible zoning uses, small bay spaces exhibit an inherently diversified tenant base, which has made the segment particularly resilient during economic downturns such as COVID-19. Our favorite strategy is to invest in small bay industrial, which is also known as small bay warehouses, light industrial, or industrial parks.

Small bay industrial units are typically anywhere from 1,500-15,000 sq. ft., and usually 25-30% of the units are comprised of office space. An asset like this might have anywhere from 3-15 separate buildings. These properties have unique zoning that provide the flexibility required by a wide variety of businesses. Permitted uses usually include light manufacturing, distribution, construction, business services, and technology. Zoning for light industrial is ideal for tenants that need multi-purpose space to host office, manufacturing, and warehousing. Leases are typically renewed for 3-5 years.

According to CBRE Econometric Advisors, small bay industrial represents about 53% of U.S. industrial space, but institutional investors own only about 2%. And only about 3-5% of industrial development activity is dedicated to small bay industrial. The construction pipeline is mostly concentrated in large distribution space. So this provides a potentially unique opportunity in an under-penetrated market segment.

I was surprised to learn that many industrial parks are owned by mom-and-pop owners. These owners typically lack the skills, desire, and resources to improve the property, increase cash flow, and maximize value.

These assets often suffer from poor management, outdated layouts and color schemes, old HVAC and windows, leaky roofs, ugly landscaping, inadequate signage, and poorly maintained parking lots. These often-absentee owners typically have significant vacancies and below-market rents. Yet no individual tenant has the negotiating power to convince the landlord to make changes. We see all this as tremendous intrinsic value potential.

Here is a graphic to help you visualize improvements at a light industrial park:

Conclusion

Do you think industrial real estate is a good investment in 2023 and in the next 5-10 years? We believe it is for us and our investors. If you have any questions, please email us at invest@wellingscapital.com or use this link to set up a call.

This article is for educational purposes only and is not to be relied upon as the basis for entering into any transaction or advisory relationship or making any investment decision. All investments involve the risk of loss, including the loss of principal. Past performance and any performance results reflected in this article are not an indication of future results.