Q3 2025 Market Commentary: rates, liquidity, and delinquencies

As mentioned in the Q1 2025 commentary posted on this blog, we plan to post every future quarterly commentary here. In the past, we shared the market commentaries with only our investors in our quarterly reports. We hope you find it helpful as you consider investing in commercial real estate!

Introduction

I’m (Paul) flying back from a commercial real estate event in Scottsdale. After spending three days with two dozen seasoned CRE operators, I’m grateful for the bullets Wellings Capital has dodged and mindful of the pain many investors still face across U.S. CRE.

Our north star remains the same: protect and grow investor capital by focusing on high-quality operating partners, historically recession-resistant asset types, and conservative underwriting.

The three primary levers in Q3 2025 were rates, liquidity, and delinquencies. Conditions remained restrictive by long-term standards, but each area showed incremental improvement for the CRE market: inflation cooled and rate volatility eased; banks remained selective but consistent; and headline delinquency measures improved slightly outside of office.

Inflation & rates. Core PCE—the Fed’s preferred gauge—continued to cool through Q3, running in the high-2s year over year by September (BEA). The 10-year Treasury (chart below) hovered in the low-to-mid 4s across the quarter after starting July near 4.4% (FRED). Lower volatility at the long end helped cap-rate expectations stabilize, even as all-in debt costs remain elevated versus 2020–2022. (Source: Bureau of Economic Analysis and FRED)

Credit Conditions. Banks reported continued tightening in CRE lending standards with subdued loan demand over the prior three months (the period corresponding to Q3), per the Fed’s October Senior Loan Officer Opinion Survey (SLOOS). In practice, bank credit stayed selective; life companies and agencies (Fannie and Freddie) shouldered more of the stabilized deal flow, while transitional assets leaned on private credit. (Source: Federal Reserve Federal Reserve)

Transactions & Pricing. Despite tight credit, deal volume improved from mid-year levels. MSCI’s U.S. Capital Trends noted a Q3 pickup versus Q2 as price discovery continued and more sellers met the market. The refinancing wall and extended maturities remain a central theme into 2026. (Source: MSCI and Seeking Alpha)

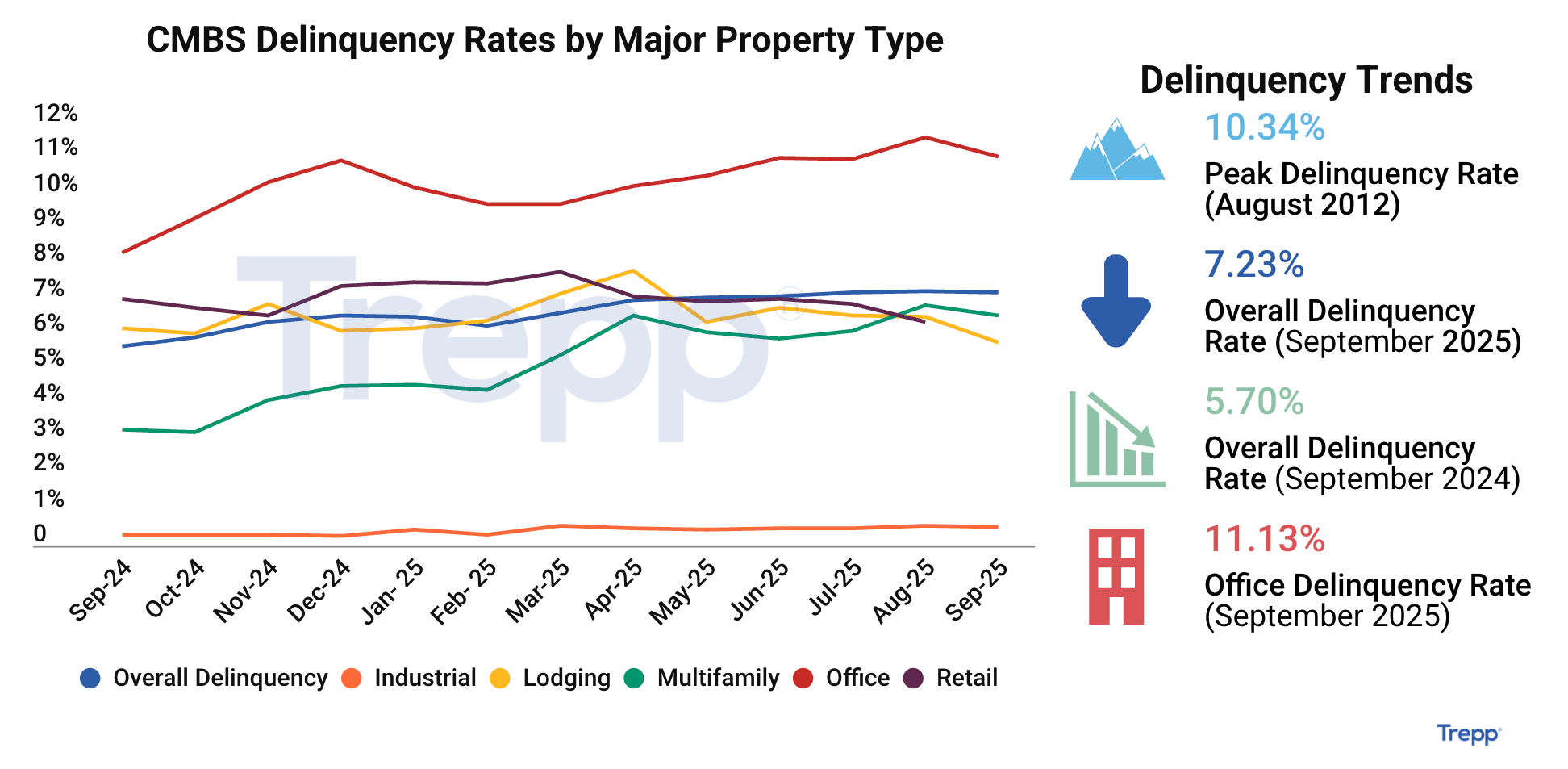

Delinquencies & Stress. In securitized debt, CMBS delinquencies edged down in September to 7.23% overall after a multi-month climb, with office properties still the outlier for distress. For other property types, delinquency rates remained materially lower than office, underscoring the dispersion in performance. (Source: Trepp and Trepp)

What Q3 2025 Meant for Our primary asset Types

Manufactured Housing Communities (MHC). Supply remains structurally constrained. Federal data show manufactured-home shipments pacing well below 2018-2021 peaks through September, limiting incremental competition while supporting steady rent trends. Limited new community development and persistent household formation at lower price points continue to underpin demand. (Source: Census.gov)

Self-Storage. After two years of normalization, the sector stabilized in Q3. Yardi Matrix reported year-over-year advertised rate growth turning slightly positive (~+0.3% in August) with improving momentum across major markets, even as operators remained tactical with promotions. With new supply moderating and seasonal softness typical into fall, the data suggest a plateau in fundamentals rather than renewed deterioration. (Source: Yardi Matrix and Yardi)

Multifamily. Rent growth decelerated as the supply wave delivered; vacancy reached ~7.1–7.2%—a series high in Apartment List’s dataset—while effective rents dipped modestly into the seasonal slow period. The near-term picture is one of absorption catching up to completions; as starts roll over, the forward setup improves, but concessions remained prevalent in high-delivery submarkets during Q3. (Source: Apartment List and Apartment List)

Industrial / Small-Bay. The industrial market found a floor in Q3: CBRE reported stabilizing vacancy alongside robust leasing and build-to-suit activity, with availability still rising but at a slower pace as construction pipelines taper. Tenant behavior favored flight-to-quality and smaller average deal sizes, consistent with an economy that is cooling but still expanding. For small-bay/flex, local service and e-commerce-adjacent demand continued to support utilization. (Source: CBRE and CBRE)

Open-Air Retail / Shopping Centers. Fundamentals held firm: CBRE’s Q3 read showed availability steady at 4.9% and net absorption turning positive for the first time this year, with modest rent growth and limited new supply. With construction pipelines thin, occupancy has been supported by expansions in daily-needs and value-oriented categories, offsetting selective closures elsewhere. (Source: CBRE)

continuing to lean into Preferred and JV Hybrid Equity

To achieve safety of principal, predictable income, and long-term growth, we’re leaning into structures that are designed to combine investor protection with opportunistic upside, a posture rooted in patience, discipline, and partnership.

We continue to favor preferred equity and JV Hybrid Equity structures that emphasize downside protection, governance rights, and disciplined underwriting while allowing participation in upside when business plans execute. In an environment of higher base rates, selective bank credit, and uneven fundamentals by sector and market, these structures can help align risk with return without relying on aggressive assumptions.

Looking Ahead

In 2023, we added preferred equity to our toolkit. Earlier this year, we introduced JV Hybrid Equity. With these structures, we’re not simply doing due diligence and allocating capital to sponsors.

We seek to take a more active role where we are negotiating deal terms, drafting the Joint Venture Agreement, and securing critical control rights like:

Forced-sale provisions

Capital improvement holdbacks

Budget approvals

Operator removal rights

Other major decision rights such as sale, refinance, and property management decisions

We now manage $450M+ AUM and $210M+ of investor equity. However, we believe ROI to our investors is more important than AUM growth.

Because of this focus, we're hiring a Director of Asset Management. The Director of Asset Management's mission is to maximize portfolio performance and net investor returns. Our goal is to control the controllable and adapt to the constantly changing market forces.

We are truly honored to steward your capital, and thank you for entrusting us as partners. If you have any questions, please contact us or use this link to schedule a call with us.

DISCLAIMER: Past performance is not indicative of future results. There is no guarantee that any forecasts or projections will be achieved. Any investment involves significant risk, including the possible loss of principal. Investors should carefully consider the investment objectives, risks, charges, and expenses of any Wellings Capital Management, LLC (“Wellings”) investment program. Offering documents containing this and other important information are available by calling 800.844.2188, emailing invest@wellingscapital.com, or visiting wellingscapital.investnext.com.

The information in this article is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction where such an offer or solicitation would be unlawful. Wellings does not provide tax, legal, or accounting advice. Investors should consult their own advisors regarding any investment. Information and any opinions contained in this article have been obtained from sources that we consider reliable, but we do not represent that such information and opinions are accurate or complete and thus should not be relied upon as such.