Q4 2025 Market Commentary: Bearish Sentiment and Improving Fundamentals

As mentioned in the Q1 2025 commentary posted on this blog, we plan to post every future quarterly commentary here. In the past, we shared the market commentaries with only our investors in our quarterly reports. We hope you find it helpful as you consider investing in commercial real estate!

Introduction

If you follow the headlines and investor sentiment, commercial real estate still seems gloomy. Higher rates linger. Office struggles dominate the news. Recession fears refuse to die quietly.

And yet, beneath the noise, the inputs that actually drive long-term real estate outcomes are quietly improving.

Last month, Blackstone President and COO Jon Gray described a market that has largely bottomed and is now beginning to recover as financing conditions improve and transaction activity slowly returns. Importantly, he also acknowledged that public market sentiment toward real estate remains deeply negative. (Source: Blackstone)

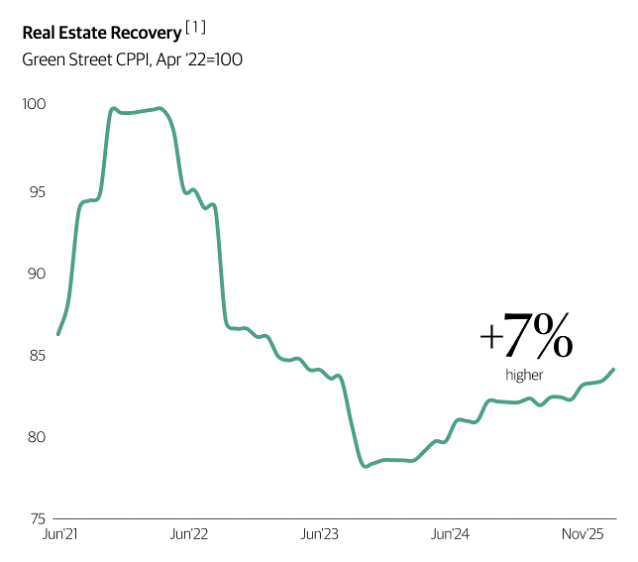

Green Street Commercial Property Price Index

That disconnect matters. Historically, some of the most attractive entry points appear when sentiment is poor but fundamentals are quietly strengthening. This could be a significantly “Buffettesque” moment in investment cycle.

At Wellings, we see at least four converging trends that make this look like we are on the verge of a positive turnaround:

Many “extend-and-pretend” multifamily loans are now breaking, with over $7 billion of multifamily loans seriously delinquent and a growing refinancing wall forcing assets to trade near or below outstanding debt balances. (Source: CRED iQ via Multifamily Dive, Q3 2025 delinquency data)

New multifamily supply has dropped and will continue to drop precipitously (see below).

The housing shortfall that began in the Great Financial Crisis continues to widen.

We believe interest rates will drop, resulting in an improvement in the CRE realm.

We believe these factors will directly lead to significant opportunities in multifamily and manufactured housing, two areas of greatest focus for Wellings Capital.

An economy that is uneven, not broken

The macro backdrop today looks more nuanced than dire. Inflation pressures appear to be easing, particularly in shelter, though official data tends to lag reality. Economic growth has remained more resilient than many expected, even as certain consumers feel strain.

This “two-speed” dynamic is real. Higher-income households remain relatively stable, while lower- and middle-income households face more pressure. That reality reinforces why we favor needs-based real estate. People can delay travel or discretionary spending. Housing, groceries, and logistics tied to daily life do not disappear.

Early innings of a cyclical recovery

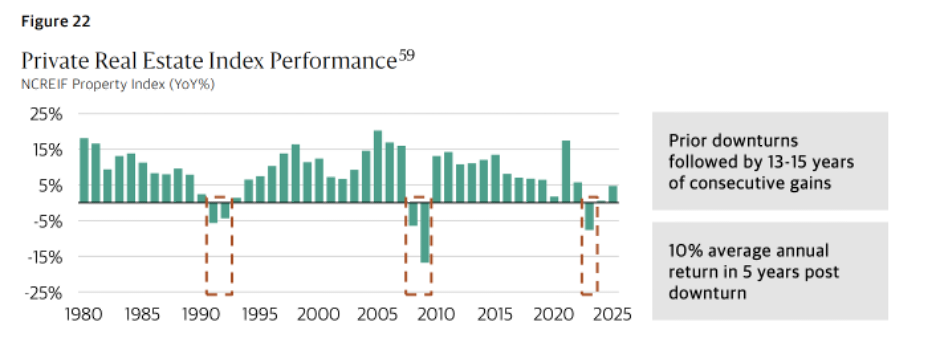

Blackstone argues that values peaked in 2022 and declined meaningfully over the next two years, with stabilization showing up by early 2024. They frame 2023 as the trough for private market values, the third major downturn in roughly 45 years. (Source: Blackstone)

Here is the historical rhyme worth paying attention to. In the prior two major downturns, the early 1990s and the Global Financial Crisis, private real estate delivered double-digit average annual returns over the following five years as fundamentals and capital markets recovered. (Source: Blackstone)

History never repeats perfectly. But it often rhymes loudly enough to be useful.

Blackstone recently summarized the current setup succinctly, noting that real estate is entering the “next phase of the cycle,” driven by reset values, improving capital markets, and tightening supply. That framing aligns closely with what we are seeing across our own deal flow.

The most underappreciated driver: collapsing construction

If there is one factor that deserves more attention, it is supply.

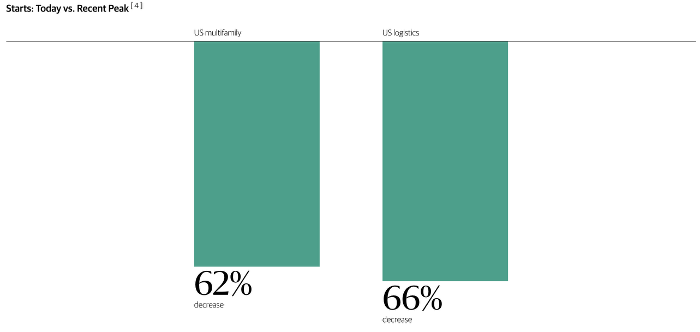

New construction across most major U.S. property types has declined sharply. Rising material costs, higher financing costs, and tighter lending standards have combined to slow development dramatically. Blackstone has pointed out that new supply across major U.S. sectors is down more than 60% from recent peaks. (Source: Blackstone)

The chart below highlights that the recent multifamily supply wave is moving through, while future starts have fallen meaningfully. Logistics construction has also pulled back significantly, setting up a more favorable supply-demand balance.

Independent research supports this trend. CBRE expects multifamily construction starts to remain well below recent highs, with improving fundamentals as the pipeline shrinks. (Source: CBRE)

CBRE Industrial research similarly shows logistics construction slowing materially after several years of aggressive development. “A sharp collapse in new construction is setting the stage for supply shortages and potentially outsized rent growth over the next three to five years. Since 2022, logistics starts are down 65% by square footage and multifamily starts have fallen 44% by units.” (Source: CBRE)

When replacement costs rise and new supply falls, existing assets often benefit over time. We expect this to benefit many of the investments in our eight existing funds and numerous sidecars.

Housing remains structurally undersupplied

Housing fundamentals continue to be one of the strongest long-term themes in U.S. real estate. We think most investors are missing this crucial point.

Blackstone’s framing is simple: the U.S. is building roughly the same number of homes as in 1960, while the population has nearly doubled, contributing to a multi-million unit housing shortfall. (Source: Blackstone)

Multiple independent studies point to a significant housing shortage. Freddie Mac estimates the U.S. is undersupplied by roughly 3.7 million homes. Brookings places the shortfall closer to 4.9 million units. (Source: Freddie Mac and Brookings.edu)

Affordability compounds the issue. According to CBRE and national housing data, owning a home is roughly 35% to 40% more expensive than renting in many markets. The National Association of Realtors reported that first-time buyers accounted for just 21% of purchases in 2024, the lowest share on record. (Source: ABC News and National Association of Realtors)

The result is persistent rental demand. This supports our continued focus on rental housing and on the less glamorous end of the spectrum, including manufactured housing communities, where supply is constrained and demand is driven by necessity rather than preference.

Why Wellings’ capital stack focus fits this moment

We believe where you sit in the capital stack matters more than ever.

Over the last several years, Wellings has intentionally focused on preferred equity and JV Hybrid Equity, prioritizing downside protection during uncertain periods. That approach remains relevant today. (Source: Blackstone)

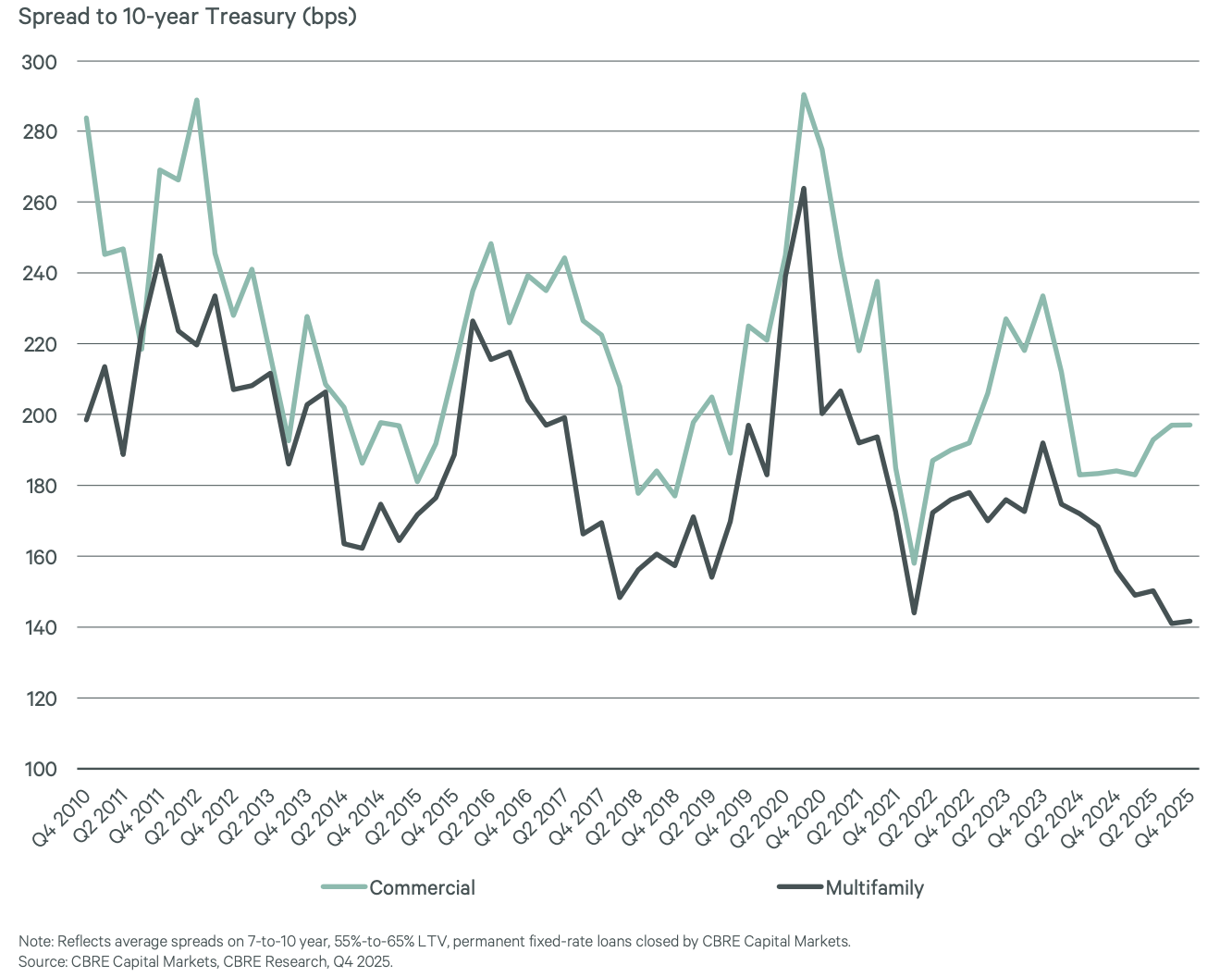

At the same time, conditions are evolving. Financing costs today are meaningfully lower than their 2023 peak, and historically, declining rates have coincided with strong real estate performance. Falling rates tend to improve equity yields and transaction activity, which we are already beginning to see.

Source: CBRE

This situation provides a positive sign for investor returns overall. But it points to declining absolute (not risk-adjusted) return opportunities for preferred equity structures.

When we started structuring preferred equity deals about three years ago, we were able to close deals with a (9 or 10% current pay plus a 6% or 7% compounding/accruing upside (15-17% total coupon) with reasonable risk. Those deals don’t exist right now. From what we’re seeing in the market today, similar preferred equity deals are pricing around a 6-7% current pay plus about 4% to 5% upside (10-12% total coupon).

When declining financing costs intersect with historically strong post-trough periods, the opportunity set broadens. For that reason, we expect to pursue more JV Hybrid Equity opportunities rather than preferred equity as the cycle matures, always with conservative underwriting and experienced operators.

Why we are not chasing data centers

Data centers are a clear beneficiary of long-term digital and AI trends, and Blackstone has been vocal about that conviction.

Our posture is intentionally different. We prefer sectors with fewer unknowns, less crowding, and less hype-driven capital inflows. Often, the best risk-adjusted opportunities live in fragmented, mom-and-pop-dominated, under-loved corners of real estate rather than in the most popular trade of the moment. Manufactured home communities are a perfect example of this.

Why “now” can be compelling for disciplined investors

We believe the setup for patient, disciplined real estate investing is improving: values have reset, financing conditions have eased from their peak, and new supply is falling across several major sectors.

That is also why the two currently open Wellings funds may be in a particularly interesting season. Early investments are made near today’s reset pricing, with potential upside as assets season and the cycle progresses.

As always, our approach remains unchanged. No hero underwriting. No blind leverage. Just conservative structures, strong partners, and a relentless focus on ROI over AUM.

We are truly honored to steward your capital, and thank you for entrusting us as partners. If you have any questions or would like to discuss how we’re viewing opportunities in the commercial real estate market, please contact us or use this link to schedule a call with us.

DISCLAIMER: Past performance is not indicative of future results. There is no guarantee that any forecasts or projections will be achieved. Any investment involves significant risk, including the possible loss of principal. Investors should carefully consider the investment objectives, risks, charges, and expenses of any Wellings Capital Management, LLC (“Wellings”) investment program. Offering documents containing this and other important information are available by calling 800.844.2188, emailing invest@wellingscapital.com, or visiting wellingscapital.investnext.com.

The information in this article is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction where such an offer or solicitation would be unlawful. Wellings does not provide tax, legal, or accounting advice. Investors should consult their own advisors regarding any investment. Information and any opinions contained in this article have been obtained from sources that we consider reliable, but we do not represent that such information and opinions are accurate or complete and thus should not be relied upon as such.